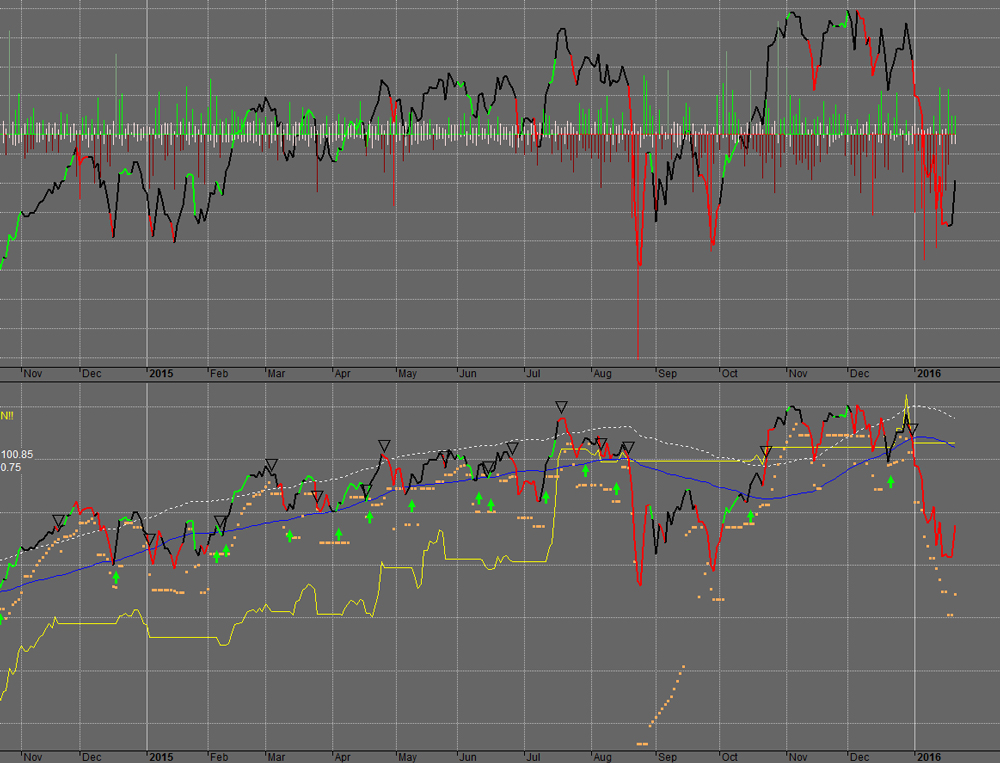

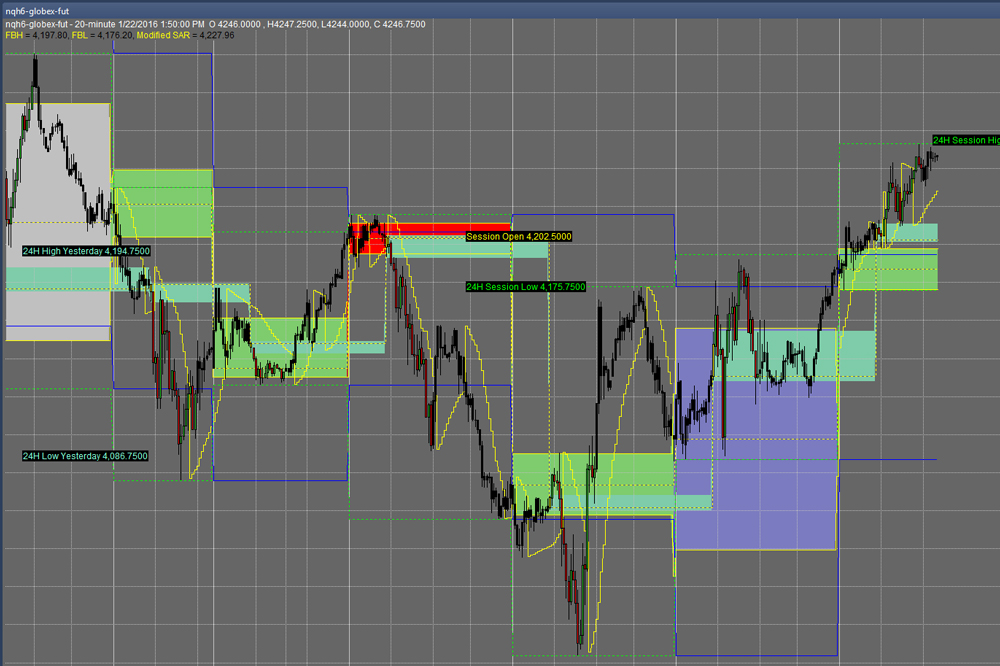

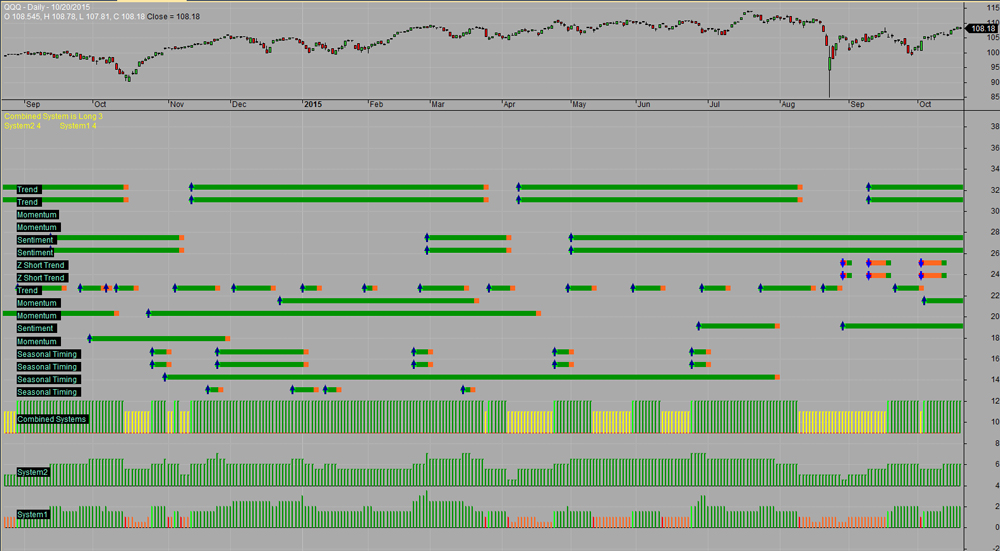

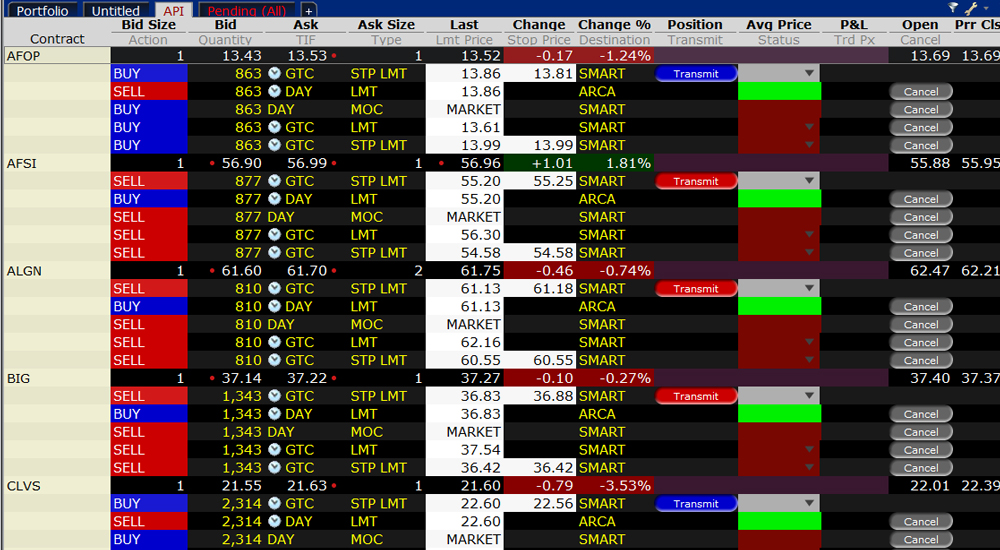

InStat Research developed out of a realization that quantifiable technical analysis is one of the best measures for evaluating price movement of financial instruments. Lead by Anthony Abry, a Chartered Market Technician (CMT), InStat Research uses Amibroker technical analysis software for a majority of its development. Below, find a sample of strategies using Amibroker, Excel, and Interactive Broker's Trader Workstation (TWS).

We optimize strategies,

develop trading apps,

provide customized backtesting,

and create automated trading strategies.